Here is a sample that showcases why we are one of the world’s leading academic writing firms. This assignment was created by one of our expert academic writers and demonstrated the highest academic quality. Place your order today to achieve academic greatness.

Table of Contents

The aim was to discuss the investment appraisal methods, and the evaluation of the investment appraisal method concerning the data set presenting the investment cash inflows and outflows over the next five years. The main purpose of undergoing investment appraisal is to evaluate and analyse different portfolio decisions and their future value.

The investment scenario had been created by looking at an investment prospect of a specific project only, which consisted of purchasing an asset and using it for five years. The asset generated inflows during the five years of use and was sold at a scrap value of 2000 pounds. The initial amount was 25000 British pounds.

The accounting rate of return came out to 34 per cent, the payback period was computed as 3 years and 313 days which is almost 4 years and the net present value of the asset invested was concluded at 10,000 British pounds approximately. Moreover, financial fraud has been the result of several companies where ethical values are not inculcated. Furthermore, some of the popular financial ethical issues that are commonly found are insider trading and campaign financing.

The complexity and uncertainty related to strategic capital investment increase the likelihood of presenting challenging situations for the investors. The utilisation of financial appraisal tools is likely to contribute to making appropriate decisions for strategic investment projects (Olawale, Olumuyiwa, and George, 2010).

The appraisal of the existing capital investments within the projects is fundamental for the success of the business organisations. The business entities experience challenges in the allocation of scarce investment resources within the manufacturing projects and processes (Gotze, Northcott, and Schuster, 2016).

The traditional business entities rely on the utilisation of capital budgeting methods for carrying out evaluation and justification within the investment-related decisions (Bouwens, 2017). In this regard, the utilisation of the investment appraisal methods contributes to analysing, evaluating, and deciding whether it is appropriate to allocate resources within the project.

This assignment aims to discuss the investment appraisal methods, and the evaluation of the investment appraisal method concerning the data set presenting the investment cash inflows and outflows over the next five years. In addition, this assignment will also present the impacts of ethical considerations on the financial decision.

Investment appraisal is defined as the methods and techniques that are used to identify the extent to which an investment is beneficial for a project or not. This involves the purchase and selling of assets. The main purpose of undergoing investment appraisal is to evaluate and analyse different portfolio decisions and their future value.

According to the study conducted by Gotze, Northcott and Schuster (2016), it was found that the primary aim or the objective of this task is to assign a value to the assets that are being purchased or sold so that their overall costs can be justified.

Several factors are taken under consideration in this case such as legal and financial issues. The overall value of an asset may help the organisation in meeting its obligations and legislation. However, it was argued by Emmanuel, Harris and Komakech (2010) that investment appraisal is mostly quantified but financial returns are received in future against it.

There are several types of techniques in investment appraisal as described in the next section. The best method for investment appraisal is the payback method. It is the time taken for the inflow to equal the investments made through cash. However, to compare different investments that are made is ARR which is expressed through the percentage of the total costs.

In addition to this, it was also determined that there are several issues encountered during the evaluation of investment appraisals. This is so because of the uncertainty of the assets and their value in future. The first issue that is raised is related to business investments that are made continuously.

The level is a risk that is involved is predicted at the initial stage as well as the outcomes. If a person intends to make any investments so they also expect to receive a return on it for which the risk factor can be ignored or mitigated. However, the risk factor also varies depending on several other factors. Some of the factors that can create risks are the length of the project (Hoesli and MacGregor, 2014).

This is so because as the time duration of the project keeps increasing so along with it, the risk element also increases. Secondly, the size of the investments made also increases the risk because when a small number of investments are made so there are fewer chances of loss.

Most of the studies that are conducted in a similar domain have highlighted that projects face more risk in investments when they have to make assumptions about costs, demand and pricing. This is so because the market changes are so rapid that they involve changes in the price and demand for products.

Therefore this exposes the high level of risks for making investments. Though the investment decisions are taken by considering the methods and techniques at the same time, they also have to consider other factors such as investment decisions and their objectives, image of the company, involvement of the stakeholders and quality of products and the services offered to the customer (Agarwal and Thakur, 2013).

Therefore, it is evident from the existing studies too that investment appraisal is a risk involving a method that gives higher returns to the investors in future. Many researchers have also stated that it involves contradictory results still it depends on the payback periods.

Professional editors proofread and edit your paper by focusing on:

The accounting appraisal method is one the most widely utilised method for understanding the payback period. This method includes the concept of net earnings and earnings excluding depreciation and tax, which is vital to consider for appraising the investment proposal (Christodoulou, Clubb, and Mcleay, 2016).

This method also provides facilitates the comparison of the new product with the cost of the other projects of a similar nature; therefore, this method demonstrates a clear picture of the profitability of the project. In addition, this method can also be effectively utilised to assess the current performance of the firm, which is another strength of this method.

Despite various advantages, the method of investment appraisal has a range of disadvantages. For instance, if the return on investment is calculated by considering ROI and ARR separately, the results are likely to demonstrate clear variation, creating difficulty in decision-making (Bouwens, 2017).

In addition, this method lacks consideration related to the time factor; therefore, ignoring the time value of the fund is a potential weakness of this method. The investment appraisal method also lacks the considerations related to the external factors and cash inflows, which are essential to be determined for assessing profitability.

The payback method is a simpler method requiring few inputs and is easy to calculate as compared to other methods used for measuring capital budgets. The utilisation of this method contributes to making quick decisions, by considering a few inputs, which is one of the potential strengths of this method.

Häcker and Ernst (2017) mentioned that the payback method does not consider the time value of money, which is a potential limitation of this method. For some projects, the largest cash flows are not likely to occur until the end of the payback period; whereas, and the payback method neglects the cash flows which are received after the payback period.

Some of the entities require the capital investments to exceed the limit of the rate of return, for reducing the risk of the decline of products (Schlegel, Frank, and Britzelmaier, 2016). The payback method is not applicable in these situations, as this method does not consider the rate of return of the project.

The net present value method considers the basic idea of depreciation within the value of the currency, and also considers the cash flows are discounted by another period of capital cost. The nest present value also demonstrates whether or not the investment is effective for the creation of value for the business organisation, as well as for the investors, which is one of the potential strengths of this method (Häcker and Ernst, 2017).

In addition, this method also considers the cost of capital and the risk inherent while making future projections. Schlegel, Frank, and Britzelmaier (2016) demonstrated that the net present value method requires assumptions related to the cost of capital of the business firm, which is one of the limitations of this method.

Assuming the very low cost of assumption is likely to result in making suboptimal investments, whereas, assuming the cost of capital very high is likely to contribute to making effective investments. For this reason, the net present value might also provide less appropriate results.

The internal rate of return considers the time value of money while evaluating the project, which is one of the most significant advantages of this method. DeFusco et al. (2015) mentioned that the internal rate of return is simple to interpret, and has been widely utilised by the managers.

Mellichamp (2017) stated that the internal rate of return is not dependent on the hurdle rate or required rate of return; therefore, the use of this method of investment appraisal further reduces the risk of decision making due to wrong calculation of hurdle return. In addition, the internal rate of return is also not based on the required rate of return, such that estimation rates can also be considered by calculating the internal rate of return.

Patrick and French (2016) mentioned that utilisation of the internal rate of the method lacks the considerations related to the project size while making the comparison between the projects. In this regard, the utilisation of the internal rate of return method reflects the smaller project as more attractive, without considering the likelihood of acquiring higher cash flows and generation of higher profits from larger products (Mellichamp, 2017). In addition, this method only emphasises the projected cash flows which are generated by the capital injection and do not consider the future cost which is anticipated to have a significant impact on the future cost.

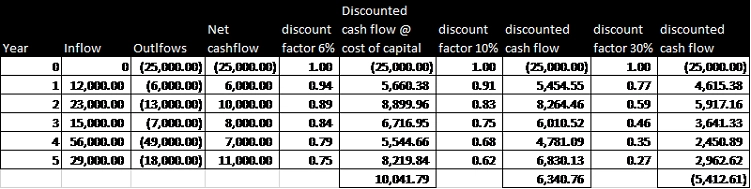

The investment scenario had been created by looking at an investment prospect of a specific project only, which consisted of purchasing an asset and using it for five years. The asset generated inflows during the five years of use and was sold at a scrap value of 2000 pounds. The initial outlay was 25000 British pounds.

The use of the asset produced positive cash flows in the form of manufacturing and selling goods produced from it as per the explanation provided in the article by Francis et al (2013). After which the asset also required costs to repair and maintain. The net cash flows had been used to estimate the returns, payback period and the net present value.

Moreover, it can be seen that the scenario used 6 per cent as the cost of capital. This percentage is usually around 5 per cent, as the company using multiple sources of funds and practices using general borrowing funds to finance its assets, ends up getting this value as a cost of capital.

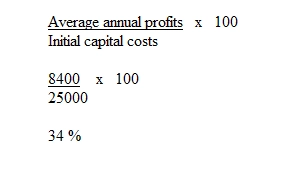

The results of the appraisal also need a discussion. The accounting rate of return came out to 34 per cent. This computation assumes that the cash flows are the profits earned by the business. In addition, there are no non-cash expenses charged for the use of the assets similar to what has been mentioned by Alin-Eliodor (2015) in the article. The return of 34 per cent over the value of the investment is sufficient. However, the same if spread over five years comes out to 7 per cent only. This is somewhat above the cost of capital.

Therefore, the project can be undertaken by the business. However, the return may not be very high and the business may not be very viable in the long run. As the business requires higher volumes of profits to run profitable operations in the future. The payback period was computed as 3 years and 313 days which is almost 4 years. The asset is used for 5 years, while the asset pays back before that period, which may seem permissible.

The net present value of the asset invested was concluded at 10,000 British pounds approximately. Having a positive NPV means there is a go at the investment. Considering all the cash flows, discounted at the business’ cost of capital, gives a positive net present value. This means that the value of inflows is more than that of the outflows, both after the due discounting. The net value of the discounted cash flows was 10041.8 pounds similar to the work of Mousavi et al (2013).

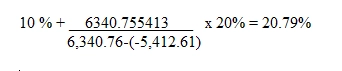

The internal rate of return is the value at which the discount rate yields the cash flows from the investment are zero. The internal rate of return (20.79%) is higher than the accounting rate of return which means that the costs used to arrive at the accounting rate of return are more than the cash flows used in arriving at the internal rate of return.

Accounting Rate of Return

Payback 3 years 313 days

Net present value (using investors’ cost of capital)

As computed in the table above = 10041.8 pounds

Internal Rate of Return

The application of investment appraisal techniques can be considered as the evaluation of the techniques that are considered for the portfolio that has been designed in this study. For the current scenario that has been created, the accounting rate of return was 34%, payback was 313 days, NPV was 10041.79 and internal rate of return was 20.79%. Based on this, it can be considered that Net present value was an appropriate method of evaluation as it provides the exact pound value of the return to be received in future.

The methods that are used for making the investment portfolio are NPV (net present value), ARR (accounting rate of return), payback and IRR (internal rate of return). All these methods and techniques are commonly used by firms to analyse and evaluate the investment appraisal techniques (Mackevičius and Tomaševič, 2010).

However, based on the existing studies that are considered, it was found that NPV is the best investment appraisal technique. This is so because the return received in future is much higher than the present value of the investment. It shows the number of pounds that it will create for the company.

Therefore, it was found from the existing studies that NPV is highly beneficial for determining what value the investment will create for the investor. Unlike the other methods and techniques, NPV takes into consideration the cost of the capital which is used in discounting the value in every period and also calculating the risk of projects (Sartori et al., 2014). The cash flows are used to predict the risk.

However, even though the firms and other investment agencies should take this into account that it is essential to not only depend on a single method such as NPV but the investment appraisal should be analysed through all methods. This is also validated by the different project portfolios where the investors not only concentrate on a single method but also consider other methods for finding the value of their assets in future (Carmichael, 2011).

Apart from NPV, the portfolio designed in this report has used other methods too such as ARR (accounting rate of return), payback and IRR (internal rate of return). The discount factor was used as 6% on each of the costs of the capital over 5 years. This indicates that for 5 years, different returns will be received on a certain amount invested which was 25000 pounds.

Ethical considerations are described as the regulations or set of morals that are diligently followed in an organisation. However, ethical principles are different for every organisation and every sector depending on the culture. Ethical considerations are particularly taken into consideration while making financial decisions because, in financial decisions, the system, rules, policies, frameworks, stakeholders, resources and even budget are considered so, ethically, the company should not get involved in any activity which is harmful to the growth of the firm.

Furthermore, it was also determined that in many business activities, several scandals take place that affects or tarnish the image of the company in the market (Pandey, 2017). These scandals raise questions about the ethical principles and morality of the firm. However, based on the different financial scenarios, it has been evaluated that the involvement of the accountants and financial managers is mainly involved in financial frauds and scandals.

Most of the financial frauds and scandals that are in limelight are the result of weak ethical principles and values embedded in employees in a firm. Reporting systems, auditing and bringing improvement in morals and ethics are some of the possible ways of eliminating this issue. Several types of financial fraud take place in organisations.

Some of the common examples of financial fraud are manipulating financial accounts of any company, misrepresenting financial information in annual reports or elsewhere, false signatures, concealing the original assets or the fixed property of the company and deliberately distributing fake documents (Parmar, 2015).

In addition to this, it was also found from the existing studies that though it entirely depends on the nature of the offence but the management has to ensure that all the employees are communicated the regulations and values. Financial fraud has been the result of several companies where ethical values are not inculcated (Skaife, Veenman and Wangerin, 2013). Furthermore, some of the popular financial ethical issues that are commonly found are insider trading and campaign financing.

Insider trading is defined as illegal misconduct of inside management of a company which buys and sells stocks within the company only and breaks the relationship of trust and confidence. Some of the studies had termed insider trading as “tipping”. On the other hand, campaign finance is defined as raising funds so that they promote political parties and organizations.

In addition to this, it was also found that such types of activities mostly destroy the name of the organisation and also they do not help the organisation in any way. Therefore, the ethical considerations should be taken into consideration so that the financial practices can be implemented accordingly.

To sum up the report, in a nutshell, it can be stated that investment appraisal is the collection and methods that are used to identify the extent to which an investment is beneficial for a project or not. It was also found from the existing studies that investment appraisal is an important technique that involves the identification of the value of an asset.

The main and most common methods that are involved in evaluating are NPV (net present value), ARR (accounting rate of return), payback and IRR (internal rate of return). All these methods and techniques are commonly used by firms to analyse and evaluate investment appraisal techniques. The current scenario taken was to purchase an asset and use it for five years. Based on it, the entire report has been evaluated.

Aggarwal, A. and Thakur, G.S.M., 2013. Techniques of performance appraisal-a review. International Journal of Engineering and Advanced Technology (IJEAT), 2(3), pp.617-621.

Alin-Eliodor, T.Ă.N.A.S.E., 2015. Statement of Cash Flows under Ro GAAP. Descrierea CIP/Description of CIP–Biblioteca Naţională a României Conferinţa Internaţională Educaţie şi Creativitate pentru o Societate Bazată pe Cunoaştere–ŞTIINŢE ECONOMICE, p.105.

Bouwens, J., 2017. Understanding investment decisions: the role of cost accounting.

Carmichael, D.G., 2011. An alternative approach to capital investment appraisal. The Engineering Economist, 56(2), pp.123-139.

Christodoulou, D., Clubb, C. and Mcleay, S., 2016. A structural accounting framework for estimating the expected rate of return on equity. Abacus, 52(1), pp.176-210.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative investment analysis. John Wiley & Sons.

Emmanuel, C., Harris, E. and Komakech, S., 2010. Towards a better understanding of capital investment decisions. Journal of Accounting & Organizational Change, 6(4), pp.477-504.

Francis, B., Hasan, I., Song, L. and Waisman, M., 2013. Corporate governance and investment-cash flow sensitivity: Evidence from emerging markets. Emerging Markets Review, 15, pp.57-71.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-VERLAG BERLIN AN.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-VERLAG BERLIN AN.

Häcker, J. and Ernst, D., 2017. Investment Appraisal. In Financial Modeling (pp. 343-384). Palgrave Macmillan, London.

Hoesli, M. and MacGregor, B.D., 2014. Property investment: principles and practise of portfolio management. Routledge.

Mackevičius, J. and Tomaševič, V., 2010. Evaluation of investment projects in case of conflict between the internal rate of return and the net present value methods. Ekonomika, 89.

Mellichamp, D.A., 2017. Internal rate of return: good and bad features, and a new way of interpreting the historic measure. Computers & Chemical Engineering, 106, pp.396-406.

Mousavi, S.M., Hajipour, V., Niaki, S.T.A. and Alikar, N., 2013. Optimizing multi-item multi-period inventory control system with discounted cash flow and inflation: two calibrated meta-heuristic algorithms. Applied Mathematical Modelling, 37(4), pp.2241-2256.

Olawale, F., Olumuyiwa, O. and George, H., 2010. An investigation into the impact of investment appraisal techniques on the profitability of small manufacturing firms in the Nelson Mandela Metropolitan Bay Area, South Africa. African Journal of Business Management, 4(7), pp.1274-1280.

Pandey, A.,2017, ETHICAL ISSUES OF FINANCIAL REPORTING.

Parmar Ms Bhumika., 2015, Ethical Issues in Accounting & Finance . – PARIPEX – INDIAN JOURNAL OF RESEARCH . Vol. 4.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Sartori, D., Catalano, G., Genco, M., Pancotti, C., Sirtori, E., Vignetti, S. and Bo, C., 2014. Guide to Cost-Benefit Analysis of Investment Projects. Economic appraisal tool for Cohesion Policy 2014-2020.

Schlegel, D., Frank, F. and Britzelmaier, B., 2016. Investment decisions and capital budgeting practices in German manufacturing companies. International Journal of Business and Globalisation, 16(1), pp.66-78.

Skaife, H.A., Veenman, D. and Wangerin, D., 2013. Internal control over financial reporting and managerial rent extraction: Evidence from the profitability of insider trading. Journal of Accounting and Economics, 55(1), pp.91-110.

Ethical considerations refer to the moral principles and values that guide decision-making, ensuring actions are fair, just, and respectful. They help navigate complex issues, balancing the interests of individuals, society, and the environment.

You May Also Like

All work is written by human writers. 100% AI free, guaranteed.

100% money back guarantee if you find plagiarism in our work.

COMPANY DETAILS