Here is a sample that showcases why we are one of the world’s leading academic writing firms. This assignment was created by one of our UK essay writers and demonstrated the highest academic quality. Place your order today to achieve academic greatness.

Table of Contents

In the early 1990s, the United Kingdom was widely regarded as one of the world’s leaders in energy deregulation. The transition from a centrally deployed Pool model to an energy-only market in 2001 appeared to adopt the trend toward more decentralized market-determined valuations. Therefore, it shocked some spectators when the new UK Government ventured into a radical reform of the architectural style of the UK power market in 2010 (Kuzemko, 2014).

Some said it disregarded the competitive market principles viewed as distinguishing the UK model, with significantly differing opinions on whether it offers a viable model for others to emulate or a warning of the dangers of resuming more significant state intervention in the market. As a result, Britain’s electricity reform is of critical importance in electricity market architecture, particularly in the case of altering the EU Targeted Household energy Framework, which insists on energy-only markets (Bouzarovski et al., 2012).

The primary reasons for Electricity Market Reform (EMR) were the anticipated closure of existing fossil and nuclear power plants, a lack of desire to invest in new gas-fired capacity, and the need to decarbonize the electricity industry without significantly boosting consumer costs. The study offered to the government was contentious, and the necessary legislation took the majority of the multi-year Parliamentary term to accomplish.

The first bids under the new method were held in 2014 (Franco et al., 2015). This essay summarises the origins and motivations for EMR, its organization, and the results until mid-2018, reflecting on the degree to which it has reached the aims of secure, sustainable, and economical energy and how it may be improved. Even in this relatively short period, the regulator has implemented significant policy changes.

Ofgem has reacted to objections of inadequate network tariff setting, and bidding results have been significantly better than anticipated, so there is every reason to be optimistic for further advances, provided they can be efficiently inspired (Martins & Miles, 2021). And it will address the question, to what extent have the changes introduced through EMR been effective in encouraging the development of more renewable electricity into the generation mix?

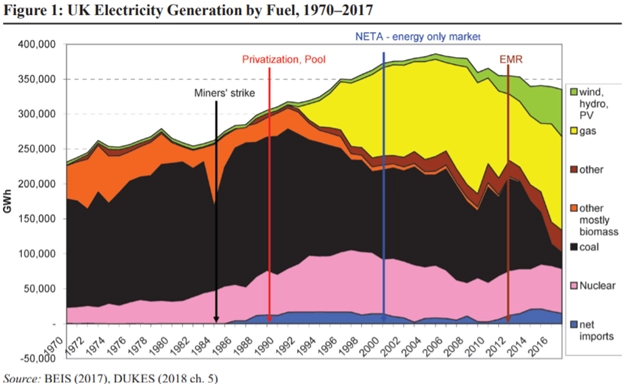

From 1950 to 2000, the UK’s power sector was state-owned, and until 1960, practically all production was generated from coal provided by the British Coal Authority. Amid government influence, oil-fired generating plants were built, and the first wave of gas-cooled Magnox nuclear power stations began operation. Figure 1 depicts the generation output by fuel and some of the significant events.

Oil’s share peaked at 40% right before the 1980 oil crisis, and after that, coal and nuclear power steadily displaced oil, with nuclear reaching 30% by 1989. By 1990, shortly after earlier reorganization for privatization, coal accounted for almost 80% of conventional thermal generating, while the percentage of oil declined from 8% to 2% in 2003 (Newbery, 2012).

Immediately after privatization, coal’s proportion fell precipitously as energy and nuclear power imports rose. It continued to fall with the ‘rush for gas,’ which was all new given the substantial excess supply. Consumption declined during the century due to economic stagnation and increasing demand efficiency. At the same time, renewables replaced coal and natural gas, whose shares were determined by the highly volatile clean (gas) and dark green (coal) flare spreads.

Figure 1 depicts the remarkable ‘rush for gas,’ with its proportion increasing from practically nothing in 1990 to over a third of generation by 2002 due to various factors. A legislative restriction on utilizing gas for power production had been repealed, and newly designed Combined Cycle Gas Turbines (CCGTs) were inexpensive, easy to build, and provided great performances, resulting in low average costs and declining gas prices.

The pool permitted new entrants to sell at the same price as incumbents, and the transparent system-wide pricing made contracts easier to negotiate. With energy policy leaving the market to lead decisions, political uncertainty was deemed minimal, and significant entry by “Independent” Power Producers (IPPs) occurred.

These engaged in long-term fixed-price contracts (and frequently shared ownership) with RECs, allowing them to pass on their expenses to the captive branded home market. Long-term energy agreements, long-term IPP agreements, regulated passthrough, and reliability assurances on CCGTs all decreased risk, while an extra motivation for RECs to accept these agreements was to capitalize on their newfound autonomy from centralized generation (Newbery, 2012). The three coal manufacturers controlled the England & Wales Pool.

They possessed significant market power, which the regulator mitigated by urging them to dispose of 6 GW of coal facilities to a third producer in 1997. The ensuing triopoly faced fewer regulatory constraints in exerting market power, and they had the incentive to do so as they saw fit. Before the “rush for gas”, coal plants’ disposal undermined their market share significantly. Indeed, coal-fired electricity had declined by more than a third by 2011 (Mitchell et al., 2011).

Reasons for altering the electrical market stem from prior complaints of the energy-only self-dispatched competitive model implemented in 2000. As time passed, ageing coal and nuclear power plants were due to close, raising concerns about finance and reliability. During times of shortage, an energy-only market pushes generators to raise their offer prices (Newbery, 2012).

In theory, investors would associate future scarcity with higher prices, encouraging them to begin investments now for fulfilment at the time of expected higher pricing. Numerous variables work against this theoretical optimism. The first is that energy futures trading is either highly illiquid or non-existent for more than a year in advance (Newbery, 2017).

In contrast, it takes 5–9 years from final equity investment to plant activation. Thus, investors must be satisfied that market circumstances over the next 25–40 years will be relatively predictable based on existing laws and regulations. Commercial rather than political forces will determine demand and supply circumstances.

Long-term Power Purchase agreements are an option for futures contracts. Still, with the end of the domestic retail brand, supply companies can no longer be convinced regarding their potential market. Thus, there were no willing counterparties to sign such contractual agreements, as there had been in the pool’s initial periods (Warren & Seal, 2018).

Even if no other factors were considered, it would take a courageous shareholder to dedicate billions upon billions to a venture with the potential outcome of rising energy prices to represent a burgeoning lack of supply. On inherently unpredictable time frames, unfathomable tiers set against dependable government pressure that would likely limit price rises (Franco et al., 2015).

In the early 2000s, there was a rising discussion among economists, primarily between abstract theory and the actual reality of ‘missing money in the calculations of prudent and risk-averse capitalists. Political turmoil was added to the inherent economic uncertainties, including future market circumstances and the expected magnitude, timing, and frequency of scarcity pricing. Investment necessitates faith in the foreseeable political climate and wholesale power prices’ drivers, which may be reasonably estimated or hedged (Warren & Seal, 2018).

Secondly, carbon price was supposed to promote the rising urgency for reducing greenhouse gas emissions and decarbonization. Convinced by the effectiveness of the US sulphur cap-and-trade programme, the European Union established the EU Emissions Trading System (ETS) to meet the EU’s Paris objectives with an EU-wide carbon tax encompassing half the total emissions (Newbery, 2016).

Nevertheless, the EU ETS has failed to provide a sufficient, long-lasting, credible carbon pricing signal. The emission levels allowance price had gone down to nil by the end of the first trading session in July 2008. While it rose to a more plausible €35/tonne CO2 in the second overtime in early 2008, it collapsed to €14/tonne with the financial crisis, alternated around that for two years, and then fell further to well below €11/tonne. The anticipated carbon price level heavily influences coal, gas, and zero-carbon generating investments. Investors have seen the EU carbon price decline four times in the last four years (Baker, 2016).

Thirdly, UK renewables legislation was similarly volatile and unpredictable. The Renewables Act (2009/28/EC) of the European Union increased the necessary contribution of renewable energy from 11% in 2011 to 21% of final energy consumption by 2021, with each nation agreeing on its target share. The United Kingdom agreed to a complicated claim; starting with one of the lowest contributions (just 2 per cent), their objective of 13 per cent entailed a massive increase in renewables (Mendelevitch & Oei, 2015).

Because power is the most superficial industry to attack, traditional production would not supply a large portion of the electrical market (at least, measured by output). The Directive also fails to withdraw permits from the EU ETS supplanted by renewables, putting additional lower pressure on the carbon price. To these contradictory signals was added a gradually rising knowledge that substantial renewables entrance, if implemented, would smash the wholesale market energy price. As a result, the rationale for traditional investment was further weakened and beleaguered (Newbery, 2016).

The other motivating factor for EMR became the requirement for low-carbon investment. Indigenously, the UK Climate Change Act 20087 was approved, providing a legal structure for the government to achieve its climate change obligations. The Act mandates that emissions be reduced by at least 85% by 2040 relative to 1999 levels, with the government committing to a series of 5-year carbon budgets (Newbery, 2016). However, the UK government’s renewables programme was a shamble.

After a decade of legislative attempts to repair nuclear power’s image, the administration also wanted nuclear facilities developed by the private sector in this liberalized electricity market. Britain was confronted with two extra challenges. The EU Large Ignition Unit Act, followed by the Industrial Emissions Directive, imposed more burdensome emissions limitations that would compel the retirement of ageing coal plants unless reconstructed in dangerous and uneconomic scenarios. Second, Britain’s first two generations of nuclear power plants were nearing the end of their operational lifespan. It was predicted that 11 GW of older coal-fired plants would shut down by 2016, and another 7.2 GW of nuclear plants would close by 2021 (Guo, 2020).

As the price of fossil fuels approached its high in 2013, the UK power paradigm became more unsustainable, as evidenced by two government evaluations. First, the UK Climate Change Committee—the organization established to oversee the implementation of the Climate Change Act—concluded that a market system based only on competitiveness for trading electrons could not provide low-carbon investment. In addition to the general worries about the market’s instability and the insufficiency of carbon pricing, energy prices based on short-run production could not sustain capital-intensive lower electricity cost zero-carbon production, whether renewables or nuclear (Newbery, 2017).

Gas production may be insured by transferring fuel costs to the market; on the other hand, zero-carbon projects would bear the entire price risk of fossil fuel and carbon pricing uncertainty. The energy-only market mechanism ran counter to the main goal of the Climate Change Act, which was to provide tactical assurance for low-carbon projects and thereby lower their substantial financing costs.

In summary, the energy market was not well-tailored to deliver a stable or viable power supply. The concept of ‘cost effective’ was questioned as retail electricity rates kept rising. At the same time, the sector was alerted about the high financing costs associated with multiple risks. Britain’s liberalization approach was considered to fail on all three primary policy priorities (Warren & Seal, 2018).

Professional editors proofread and edit your paper by focusing on:

The following policy document established an academically consistent foundation for power market reform using four strategies. A Carbon Floor Price would rectify the lack of an actual carbon price, introduced quickly by HM Treasury in the March 2011 Spending plan. Coal and gas used to produce energy would be taxed to raise the minimum CO2 price to £16/metric ton in 2014, growing exponentially to £30/tonne in 2020, and expected to increase to £70/ton ton by 2030.

The ETS forward price was hovering at €15/tCO2 (£12/tCO2) for two years, although EMR regulation was prepared in 2010–11, and the rate was established in proportion to these levels. It meant a CPS top-up of a few pounds per ton of CO2 in 2013, with a gradual increase. However, because of the fall of the ETS cost in 2011, the CPS necessary by statute by 2013 climbed quite quickly (Grubb & Newbery, 2018).

Because any tariff might be altered with each budget, this idea was bolstered by a Carbon Quality Standard (CQS). It would restrict CO2 emissions from any primary power plant to 500 gm/kWh “at baseload,” thereby ruling out any unchecked petroleum plant. These two processes were pretty simple in terms of policy formulation.

The more challenging concerns included effectively encouraging low-carbon investment and ensuring system security. The UK’s emissions and renewables objectives are expected to necessitate more than £9 billion in annual expenditure. It was much more than financial analysts’ predictions of the Big Six’s ability to finance, necessitating new funding sources (Mason et al., 2021).

Because zero-carbon generating has significant capital costs and low operating costs, its prices are vulnerable to the Weighted Average Cost of Capital. By 2021, the aggregate investment in generating alone would be worth £80 billion, and if the WACC could be cut by 4%, consumer costs would be lowered by £3.35 billion per year. Lower risk allowed for more debt, making this easily viable. Because the Renewable Obligation system imposed all spot price and regulatory risk on companies, substituting it with a fixed-term contract would significantly decrease risk and stimulate new funding and participation (Grubb & Newbery, 2018).

The fourth component of EMR was aimed at the security of energy supply via a Capability Framework. After extended debate and research into international exposure, the government dismissed the payouts sought by newcomers. Or ones set to retire plants from the general market to pursue system-wide payouts to all generating units who could agree to produce whenever the System Operator, National Grid, called on them (Dell’Aquila et al., 2020).

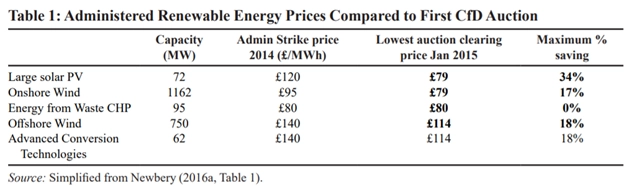

Because the law had been in the works for so long, by the time it reached its late phase in 2013, both the nuclear and renewables businesses were antsy, complaining of dwindling trust, motivation, and capacities in the UK market. Parallel to the legislative schedule, the administration negotiated an initial round of contracts for renewables and the first fleet of new nuclear power plants (Newbery, 2021). Table 1 summarises the first ‘Administrated contracts’ for renewables, which comprised 15-year contracts for wind energy at strike rates of £100/MWh (onshore) and £130/MWh (abroad) (offshore).

Furthermore, the escalating cost of the energy transition, notably CfD contracts for offshore wind, has put EMR under significant political pressure. Nevertheless, the arguments that led to the EMR gaining more significance were bolstered by the fact that exceeding the tax cap was a sign of success in providing renewables—more capacity (PV) with higher production (wind) than anybody anticipated.

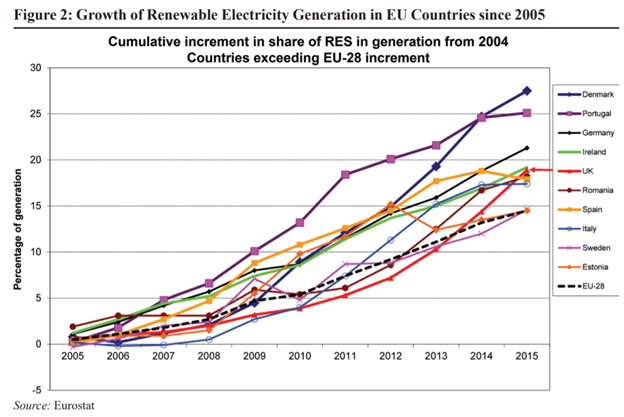

Indeed, the renewables target for electricity (30% by 2020), primarily regarded as unrealistically ambitious at first, appeared to be becoming more feasible (Grubb & Newbery, 2018). Figure 2 depicts the percentage growth in the proportion of renewable generation since 2005 (the beginning points were highly varied, partly due to pre-existing levels of hydro and biomass) for the ten EU nations whose rise was more than the EU average. Until 2010, the UK was behind most of the group but has subsequently caught up.

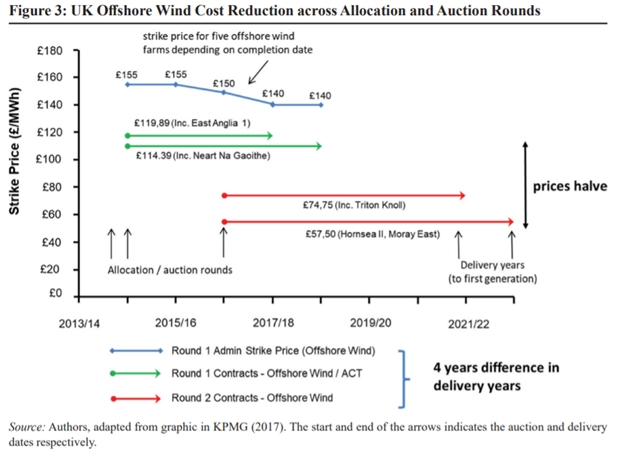

Despite sector lobbying for policy consistency and no severe alternative to EMR provided, the new government eventually declared its intention to proceed. Nonetheless, it took almost two and a half years from the first CfD auction in 2015 for the second one to take place in September 2017. And because the ‘pot 1’ auctions for technology advancements were legally obliged to include wind energy. The government devised the simple, ironic, solution of announcing that no funds would be accessible in bids for the lowest-priced renewable sources. The second bid would concentrate solely on the less developed ‘pot 2’—which included wind farms.

And the result was surprising but pleasant. Figure 3 compares the prices acquired in the December 2017 bid for three giant wind energy projects to the regulated and first bid rates. The most notable were two different power stations bringing the total 2,400MW capacity, scheduled for delivery by 2022/23 at a contract price of £56.60/MWh—far below any anticipations, at half the cost in the first bids, and allowing the government to secure 60 per cent more capacity for 50 per cent less estimated subsidy than in round 1 (Warren & Seal, 2018).

More than a quarter-century of innovations in UK energy policy have had a dramatic influence, as seen by the long-term history of fuel supply and demand. With the rush for gas in the 1990s, the United Kingdom had shifted to a roughly equal mix of coal, gas, and nuclear energy. As the earliest nuclear reactors were deactivated in the 2000s, the system was kept afloat by an excess of gas, stabilizing demand, and the sluggish growth of renewables—still hardly noticeable in overall statistics—while coal retained the primary source of baseload production and cyclical rescheduling.

In the last quarter-century after privatization, coal dropped from two-thirds of generation in 2000 to 40 per cent in 2017 and 7 per cent in 2018, halving CO2 emissions from electricity generation. Coal will be more restricted to fulfilling winter peaks in the coming years. Renewable sources, including the transformation of some coal to bioenergy, began to accelerate more rapidly in 2013, introducing feed-in tariffs for small sources and long-term CfD contracts for significant sources.

Energy consumption on the transmission system began to diminish, and by 2015, carbon price support had pushed coal to the margins of what was left. The equilibrium between the public and private sectors is being reconsidered, and we are still a long way from a realistic nuclear plan. More adjustments might enhance the support of zero and low-carbon generation, and improved location indications are still required for investments and delivery. The data shows that the UK’s EMR was a significant step forward, but there is still a long way to go.

Baker, F., (2016). Have technology-specific measures for the UK electricity market reform gone far enough? J. Clean Energy Technol, 4(2).

Bouzarovski, S., Petrova, S. & Sarlamanov, R., 2012. Energy poverty policies in the EU: A critical perspective. Energy policy, Volume 49, pp. 76-82.

Dell’Aquila, M., Atzori, D. & Stroe, O., 2020. The Role of Policy Design and Market Forces to Achieve an Effective Energy Transition: A Comparative Analysis Between the UK and Chinese Models. In. The Geopolitics of the Global Energy Transition, pp. 227-255.

Franco, C., Castaneda, M. & Dyner, I., 2015. Simulating the new British electricity-market reform. European Journal of Operational Research, 245(1), pp. 273-285.

Franco, C., Castaneda, M. & Dyner, I., 2015. Simulating the new British electricity-market reform. European Journal of Operational Research, 245(1), pp. 273-285.

Grubb, M. & Newbery, D., (2018). UK electricity market reform and the energy transition: Emerging lessons. The Energy Journal, 39(6).

Guo, B., 2020. The British Energy Market Reform: Carbon Prices, Retail Tariffs, and Cost Passthrough (Doctoral dissertation, University of Cambridge).

Kuzemko, C., 2014. Politicising UK energy: what’speaking energy security’can do. Policy & Politics, 42(2), pp. 259-274.

Martins, J. & Miles, J., 2021. A techno-economic assessment of battery business models in the UK electricity market. Energy Policy, Volume 148, p. 111938.

Mason, K., Qadrdan, M. & Jenkins, N., 2021. Investing in generation and storage capacity in a liberalized electricity market: An agent based approach. Applied Energy, Volume 294, p. 116905.

Mendelevitch, R. & Oei, P., 2015. Consequences of the UK energy market reform on the development of Carbon Capture, Transport, and Storage. In 2015. 12th International Conference on the European Energy Market (EEM), May.pp. 1-6.

Mitchell, C., Woodman, B., Baker, P. & Aldridge, J., 2011. Response to the electricity market reform consultation. Energy Policy Group, University of Exeter.

Newbery, D., 2012. Progress on the UK Electricity Market Reform. Cambridge Electricity Policy Research Group Working Paper, Volume 2307.

Newbery, D., 2012. Reforming competitive electricity markets to meet environmental targets. Economics of Energy & Environmental Policy, 1(1), pp. 69-82.

Newbery, D., 2016. Towards a green energy economy? The EU Energy Union’s transition to a low-carbon zero subsidy electricity system–Lessons from the UK’s Electricity Market Reform. Applied Energy, Volume 179, pp. 1321-1330.

Newbery, D., 2017. Tales of two islands–Lessons for EU energy policy from electricity market reforms in Britain and Ireland. Energy Policy, Volume 105, pp. 597-607.

Newbery, D., 2021. Reforming Renewables support mechanisms.

Warren, L. & Seal, W., 2018. Using investment appraisal models in strategic negotiation: The cultural political economy of electricity generation. Accounting, Organizations and Society, Volume 70, pp. 16-32.

Higher electricity production can fuel economic growth by providing reliable power for industries, businesses, and homes, stimulating production and innovation. It enhances productivity, attracts investments, creates jobs, and enables the development of new sectors like electric vehicles and renewable energy, boosting overall economic activity.

You May Also Like

All work is written by human writers. 100% AI free, guaranteed.

100% money back guarantee if you find plagiarism in our work.

COMPANY DETAILS